Viridian Reports a Substantial Increase in Cannabis M&A Deals

LOS ANGELES – Merger and acquisition (M&A) activity in the legal Cannabis sector posted a notable year-over-year increase in Q1 2026, according to the Q1 2026 Cannabis Deal Tracker Report published by Viridian Capital Advisors, the New York-based investment bank and data services firm that has tracked Cannabis capital markets transactions since 2015.

Operators Shift Strategies – Deal Volume Climbs

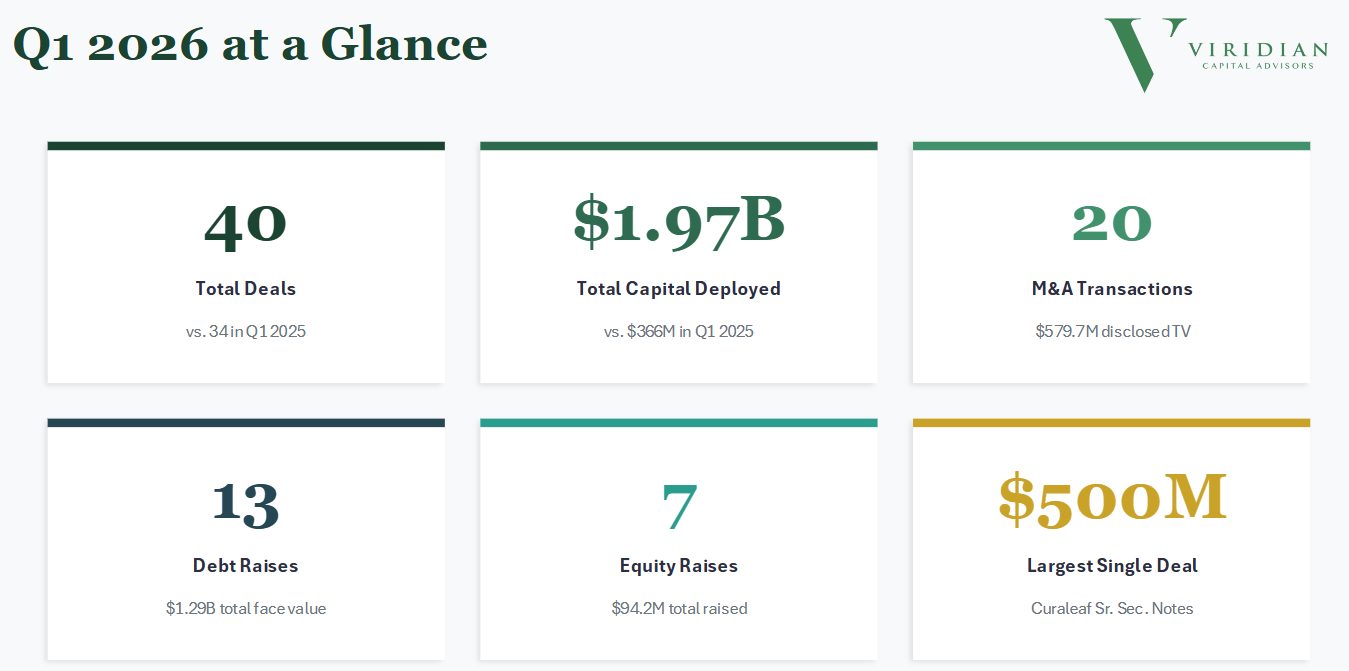

The report, which draws on a forecast and database covering more than 2,500 capital raises and 1,000 M&A transactions across Cannabis and hemp, points to a broad uptick in deal-making that cuts across both public and private company transactions. Viridian analysts documented 40 transactions across M&As, equity raises, and debt deals, with total capital deployed reaching approximately $1.97 billion. This marked a clear step up from the $366 million across 34 deals in Q1 2025.

There were 20 transactions in the quarter, compared with 12 in the year-ago period. Disclosed deal value totaled $579.7 million, a substantial increase from $38.3 million in Q1 2025. Key examples included Organigram Holdings’ acquisition of Germany’s Sanity Group, valued at roughly $261 million plus a $134 million component, and Millstreet Credit Fund’s $130 million purchase of Cannabist’s Virginia operations.

California led target activity with six deals, followed by Colorado with three. The transactions reflected several patterns: consolidation among MSOs, sales of non-core assets by companies under pressure, and select cross-border moves into European medical Cannabis markets. Private acquirers handled 14 of the 20 deals, underscoring their growing role relative to public companies.

The surge stands out against the backdrop of a sector that has spent much of the past two years working through debt refinancing pressures, federal policy uncertainty, and compressed valuations. That operators are choosing to transact at higher rates now suggests a strategic recalibration: scale through acquisition rather than organic build, particularly as MSOs weigh the cost and timeline of entering new markets from scratch.

Capital Structure Shapes the Buyer Pool

Viridian’s data framework provides important context for reading the M&A uptick. Public companies have accounted for the dominant share of capital activity, with public-company raises representing over 91% of total raises in the last twelve months – the highest proportion in at least seven years.

Debt has also become the primary vehicle for financing, comprising more than 90% of capital raised on a worldwide basis year-to-date in 2026, compared to roughly 50% in the prior year. Debt activity drove much of the overall dollar volume, with $1.29 billion raised across 13 transactions. Major refinancings by Curaleaf ($500 million), Verano, Jushi, and Canopy Growth highlighted large operators’ efforts to extend maturities and strengthen balance sheets. Equity raises stayed limited, totaling $94.2 million across seven deals, with Organigram’s $47.6 million private placement accounting for more than half the total.

That debt-heavy capital structure has direct implications for M&A. Companies carrying significant leverage – Viridian’s Credit Tracker places several operators above the 3x debt-to-EBITDA threshold it identifies as the boundary of sustainability in a 280E tax environment – face constrained optionality. For those operators, selling assets or accepting acquisition offers can become a more rational path than competing for new debt issuance. Conversely, well-capitalized acquirers like GTI, Trulieve, and Verano, which Viridian places in the lower-leverage quadrant of its financial health framework, are positioned to use their balance sheets opportunistically.

However, the surge in debt refinancings at coupons between roughly 9.5% and 12.5% shows lenders’ willingness to back scaled operators while still pricing in sector-specific risks. M&A values for disclosed deals suggest acquirers are paying up for strategic assets, particularly those positioned for potential regulatory tailwinds like Virginia’s adult-use rollout. Yet the low disclosure rate on M&A and the continued restraint in equity issuance indicate that full market normalization has not arrived. Smaller operators remain challenged, contributing to a bifurcation between well-capitalized leaders and the rest of the field.

Cultivation & Retail Lead Transaction Activity

Consistent with prior reporting periods, the cultivation and retail subsector has driven the most M&A consideration. Viridian’s Cannabis Deal Tracker places cultivation and retail at the top of both capital raised and deal volume across the twelve subsectors it monitors, with the Infused Products and Extracts segment ranking second in total M&A consideration.

Geographically, the Northeast and Central states are drawing a disproportionate share of activity. Massachusetts leads all U.S. states in total capital raised over the last twelve months, followed by New York and Illinois – states where regulatory frameworks have created viable commercial markets but where supply-demand dynamics still reward scale. California, by contrast, leads in transaction volume, reflecting the state’s fragmented operator base and ongoing consolidation among smaller license holders.

Rescheduling & the 280E Overhang

Any analysis of the Q1 2026 M&A environment requires accounting for the federal policy backdrop. Viridian has highlighted that the aggregate unpaid 280E tax liabilities across the top MSOs exceed $2 billion, a figure that in many cases surpasses both EBITDA and market capitalization. The resolution of these liabilities, which would follow any formal federal rescheduling of Cannabis, remains the industry’s most consequential open variable.

The prospect of rescheduling has contributed to a meaningful recovery in Cannabis equity prices. The MSOS ETF has posted strong gains on rescheduling-related news flow, but market participants remain cautious about timing and degree of benefit. Viridian’s analysis suggests that 280E liabilities are unlikely to simply disappear upon rescheduling and will more probably require negotiated settlement or statute-of-limitations resolution, as illustrated by the Harborside precedent. This uncertainty colors the risk calculus for any deal negotiated today that embeds assumptions about post-rescheduling economics.

Wrap-Up

The acceleration in Cannabis M&A documented by Viridian reflects a market entering a new, more mature phase of consolidation, one driven less by growth optimism than by financial necessity and strategic positioning. Operators with fortress balance sheets are acquiring distressed or subscale competitors at valuations that were unthinkable two years ago. Those on the wrong side of the leverage spectrum are running out of runway.

For capital allocators and investors, the sword forged by higher M&A volume is a double-edged one: activity increases but so does selection risk. The winner’s circle in this consolidation cycle will be defined by who controls the most defensible markets, carries the most manageable debt load, and is best positioned to absorb the 280E liability question on favorable terms. Viridian’s data, which has tracked more than $65 billion in aggregate Cannabis transactions since 2015, remains among the clearest windows into how that outcome is taking shape.

Source: Viridian Capital Advisors・Cannabis Deal Tracker・Data via dealtracker.viridianca.com

Photos & images: Viridian Capital Advisors・Pinterest ・Esquire Magazine/The Pharm

About the Author: HCN News Team

Related Posts