Whitney Economics Updates Review of Federal Tax Pressure on Legal Cannabis Operators

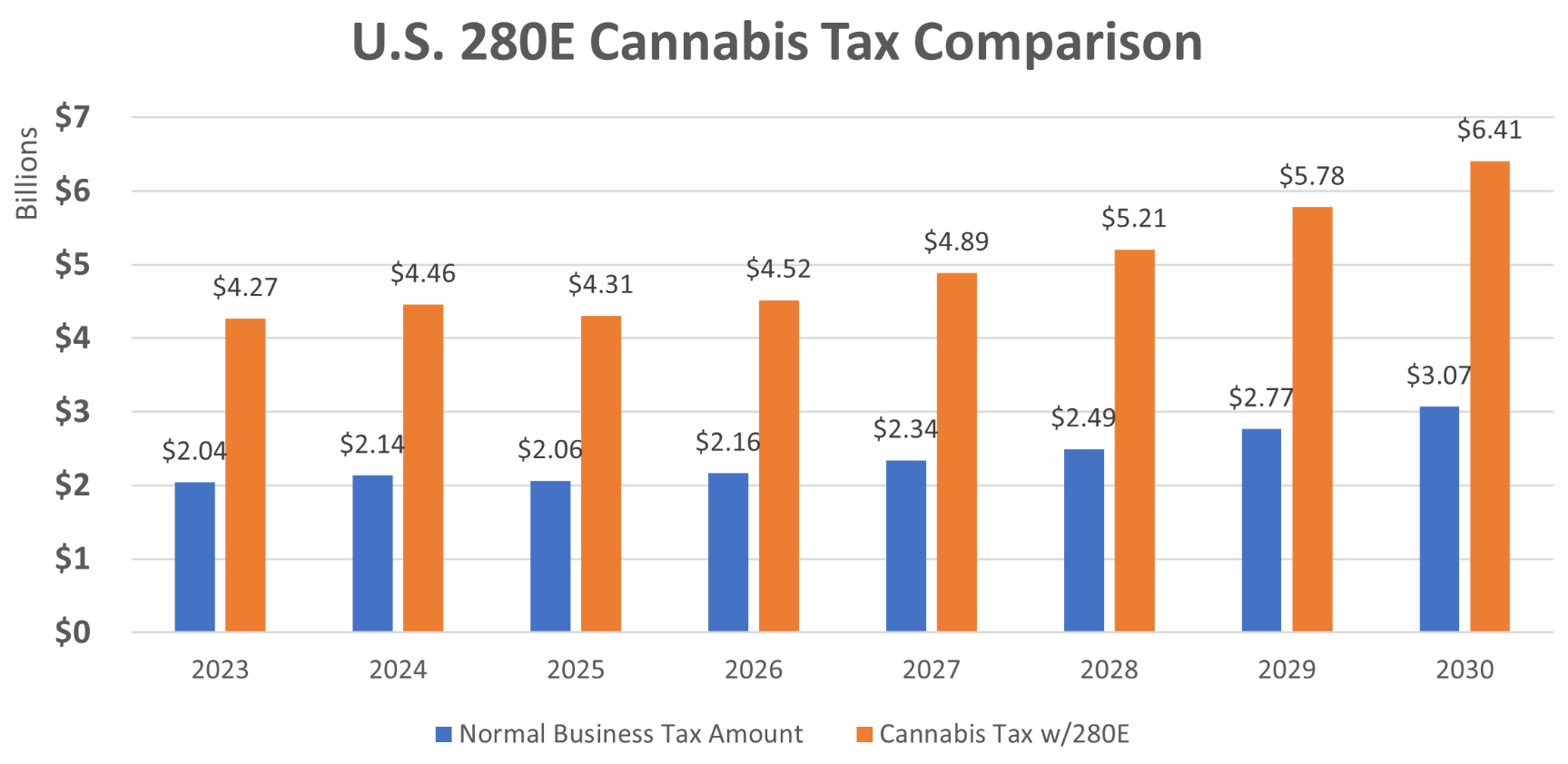

PORTLAND – Whitney Economics refreshed its analysis on the federal tax burden facing state-regulated legal Cannabis operators, estimating that they paid $2.24 billion in excess taxes in 2025 alone due to Section 280E of the Internal Revenue Code.

“The amount of additional taxes Cannabis operators pay is staggering. In 2025, there was an estimated $2.24 billion in excess Cannabis-related federal taxes due to the IRS’s 280E tax policy. The industry is being taxed out of business”, said Beau Whitney, Chief Economist at the Portland-based research firm.

Since Cannabis is still classified as a Schedule I substance under the Controlled Substances Act, licensed operators cannot claim standard business deductions on their federal tax returns. This means that costs for labor, legal fees, marketing, security and banking remain non-deductible, pushing effective tax rates to 70% or even higher for many Cannabis businesses. The recent update builds on earlier work from the agency. Since 2018, the sector has paid more than $27 billion in federal taxes altogether, with roughly $15 billion of that tied directly to the 280E restriction.

Whitney Economics noted that the original purpose of the rule was to penalize illicit drug activity. Yet, the provision still governs state-licensed operators even as those markets have matured and expanded. At the same time, widespread price declines in major Cannabis states have reduced state tax collections, prompting some legislatures to consider higher excise rates. The combination leaves many businesses squeezed on two fronts.

Rescheduling Cannabis to Schedule III would remove the 280E restriction, according to the analysis. Such a step could improve cash flow, lift profitability and make the sector more attractive to investors. Whitney called reform a question of timing rather than likelihood, though he cautioned that near-term certainty remains low.

For now, the firm is advising Cannabis operators to maintain strict financial discipline. “Too many operators may be counting on this reform for their survival,” Whitney said. “They need to stay the course but be prepared to pivot quickly once the tax policy change occurs.” Beau Whitney also pointed to ongoing price compression across major markets as an added pressure. “With pricing compression occurring in every major U.S. Cannabis market, tax revenues will no longer be the goose that laid the golden egg,” he said. “In fact, declining state Cannabis tax revenues are resulting in state Cannabis tax increases, which will further hurt revenues, making the overall tax situation untenable for the industry.”

The analysis arrives as the regulated market navigates its first year-over-year revenue decline in 2025, with Whitney Economics projecting a modest rebound to $30.5 billion in 2026.

The refreshed data illustrates a clear gap between federal tax rules written for a different era and the realities of today’s state-regulated Cannabis economy. Operators continue to absorb costs that conventional businesses do not face, while state governments weigh revenue needs against the risk of further eroding legal-market participation. While offering no predictions on legislative timelines, the analysis does supply a new benchmark for gauging how long the current tax structure can remain in place before broader adjustments become unavoidable.

Images: whitneyeconomics.com

About the Author: HCN News Team

Related Posts