UK Medical Cannabis H1 2025: The Market Still Running on Trust

LONDON – You won’t find the echoes of this revolution in the National Health Service (NHS) waiting lists or General Practitioner (GP) surgeries. It lives instead in a constellation of private clinics spread across the country, in carefully labelled jars of flower, in the inboxes of tens of thousands of patients who, until recently, had no legal route to the medicine they needed. The UK’s medical Cannabis market has arrived, and the data, compiled together, reveals a storyline of equal parts triumph and tension.

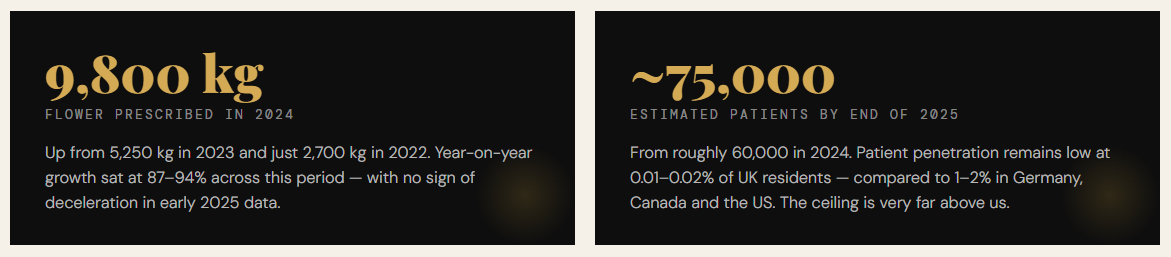

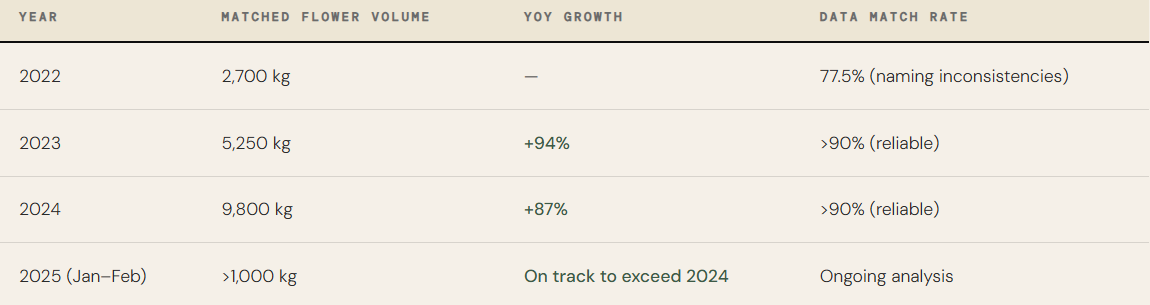

The headline is remarkable. Prescribed flower volume grew by 262% between 2022 and 2024, climbing from roughly 2,700 kilograms to nearly 10,000 kilograms. Prescription counts more than doubled in a single year alone – from around 283,000 in 2023 to 659,000 in 2024. Early 2025 figures suggest the trajectory hasn’t flattened. January and February combined exceeded a full ton of prescribed flower, pointing to annualized volumes that will dwarf what came before.

These are not abstract numbers. They represent real people: patients living with chronic pain, PTSD, multiple sclerosis, insomnia, and a dozen other conditions, who’ve found, through private prescriptions, a treatment that works for them. But they also illuminate a system operating without a safety net, built on private infrastructure, shaped by market forces, and increasingly blind to the data it is generating.

A Market That Doubled & Is Doing It Again

When Parliament amended the Misuse of Drugs Regulations in November 2018, allowing specialist doctors to prescribe Cannabis-based products for medicinal use (CBPMs), the country’s response was cautious, almost timid. NHS trusts were slow to act, clinical guidance was sparse, and prescribers were hesitant. The market limped rather than sprinted into existence.

That changed somewhere around 2022. Private clinics, freed from the institutional caution of NHS gatekeeping, began to proliferate. Economies of scale brought prices down. And patients, many of whom had been self-medicating illegally for years, began arriving in numbers that surprised even industry insiders. By April 2023 to March 2024, the Care Quality Commission recorded 346,600 items of unlicensed CBPMs dispensed by independent services, a 130% jump over the prior year.

What is driving this? Several forces are converging. Private clinics have dramatically lowered the barriers to entry: streamlined onboarding, competitive pricing, and increasingly confident prescribers have expanded the patient pool. Simultaneously, larger average prescription sizes suggest existing patients are consuming more. This is market expansion and market deepening happening simultaneously.

The UK’s market is now valued at over €300 million and is widely projected to reach €619 million by 2029, with patient numbers approaching 190,000. By those metrics, this is no longer a niche. It is a sector.

Even with patient numbers at 75,000, only 0.01–0.02% of UK residents have tried a medical Cannabis prescription. Compare that to 1–2% in Germany, Canada and the US. The ceiling is extraordinarily far away.

The Race to the Top: Higher THC, Higher Stakes

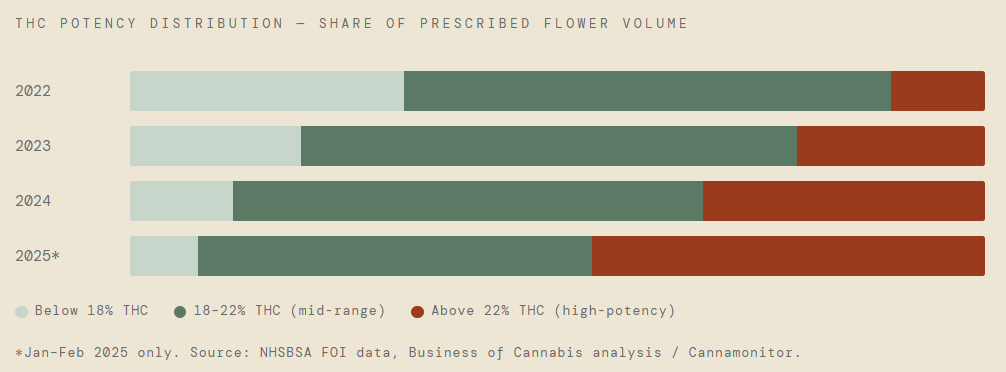

Perhaps the most striking finding in the H1 2025 data, and the one most likely to drive regulatory attention, is the dramatic, accelerating shift towards higher-potency Cannabis products. In 2022, most prescribed flower sat comfortably in the middle of the potency spectrum. Roughly 57% of matched volume fell between 18–22% THC. Only 11% exceeded 22% THC. These were, broadly, moderate-strength medical products consistent with a cautious, newly opened market.

By the first two months of 2025, products above 22% THC made up almost half of all matched volume. The mid-range products [long the backbone of the market] had hemorrhaged market share, not because fewer were dispensed in absolute terms, but because the high-potency segment had grown so explosively that it reshaped the entire scene.

This is, on one level, simply the market responding to patient preferences. Patients, many of them managing severe chronic pain, tend to want effective medicine, and in the absence of robust clinical guidance differentiating products by indication, higher THC becomes a proxy for “stronger.” Prescribers follow the path of least resistance.

A Clinical Note of Caution

Higher THC does not reliably provide greater analgesia. As discussed at the 2025 Cannabis Health Symposium, the assumption that more potency equals more efficacy is not well-supported by clinical evidence. Yet the market is behaving as though it does – a divergence between patient demand and clinical reality that deserves serious attention from prescribers and regulators alike.

The parallel to recreational Cannabis markets is uncomfortable but unavoidable. In 2022, just 3% of flower prescriptions were for products exceeding 24% THC. By 2023, that figure had risen to 22% [!]. The direction of travel is clear. Whether it reflects genuine clinical need or a quasi-recreational gravitational pull is a question the industry has not yet grappled with honestly.

A Private Ecosystem & Its Fault Lines

The UK’s approach to medical Cannabis is, by European standards, unusual: it is almost entirely privately funded, privately operated, and privately prescribed. The NHS, despite being constitutionally willing to refer patients elsewhere, has itself issued fewer than five Cannabis prescriptions. More than 99% of all CBPMs reach patients through private clinics.

This has created a market that moves fast. Forty-plus private clinics are now actively prescribing. Prices have fallen as competition has intensified. New patients can go from initial inquiry to first prescription in a matter of weeks – a stark contrast to the years-long waits many face for NHS specialist appointments. The private system has, in a real sense, democratized access to a medicine that was theoretically legal for everyone but practically available to almost no one.

But the private model also creates structural vulnerabilities. A striking concentration of prescribing power sits at the top: just ten doctors prescribed over half of all medical Cannabis treatments issued between 2019 and early 2025 – more than 805,000 Cannabis treatments combined. A single consultant was responsible for 10% of all Cannabis medicines prescribed, dispensing approximately 46,000 items in the first five months of 2025 alone. That is one prescription roughly every two working minutes.

Of approximately 100,000 doctors on the GMC Specialist Register who are legally permitted to prescribe Cannabis, fewer than 180 are actively doing so, i.e. less than one-fifth of one percent.

The prescriber bottleneck is existential for long-term growth. The market cannot safely or sustainably scale on the shoulders of a handful of doctors, however committed they are. Lack of training, institutional caution, and the absence of updated clinical guidelines are keeping the vast majority of eligible prescribers on the sidelines.

Flying Blind: The UK’s Chronic Data Problem

Any honest account of this market must grapple with a foundational absurdity: one of Europe’s biggest medical Cannabis markets has almost no reliable data about itself.

Unlike Germany, Australia, or Canada, the UK has no centralized tracking system, no mandatory product registry, and no standardized naming conventions. Clinics, pharmacies, and importers all record information differently, often relying on free-text fields rather than structured inputs. NHSBSA has confirmed that private unlicensed Cannabis prescriptions are “manually recorded from often handwritten prescriptions,” with “no standardized naming convention for the product names, strength, or volume.”

The raw dataset underlying the most recent analysis contained over 132,000 data points. The same product appeared dozens of times under slightly different descriptions. Analysts at Business of Cannabis spent considerable effort simply reconstructing a coherent picture, building a canonical product dictionary, normalizing FOI entries, and applying fuzzy-matching with potency and brand constraints to identify real, verifiable products. Even then, 2022 data could only be matched at a 77.5% rate.

This isn’t merely a bureaucratic inconvenience. The absence of reliable data makes it harder to argue for greater NHS access, harder to identify safety signals, harder to conduct meaningful research, and harder to hold bad actors accountable. It gives a systematic commercial advantage to those with enough private data to extract insights — the larger clinics and well-funded suppliers — while leaving smaller operators and patient advocates working in the dark.

In Germany, prescriptions are tracked in real time. In Canada, Health Canada publishes monthly production and sales data. The UK, which has positioned itself as a leader in evidence-based healthcare, is running one of its fastest-growing medical sectors on handwritten prescriptions and best-effort data cleaning. It is, to put it plainly, not good enough.

The Road to Maturity

The H1 2025 data is, ultimately, a portrait of a market in adolescence. The bones are strong: patient demand is real and growing, clinical evidence is accumulating, and the private sector has demonstrated that access is achievable at scale. But the market has the habits of its youth: concentrated supply, concentrated prescribing, concentrated potency preferences, and a chronic allergy to the kind of data transparency that mature sectors take for granted.

The signals from early 2025 are encouraging. The first UK medical Cannabis grower licensed to supply clinics for direct patient treatment began doing so in 2025, and has already expanded its range. Domestic cultivation capacity is building. New entrants are arriving. And despite no shift in NHS willingness to prescribe, several NHS trusts are actively referring patients to private clinics – an acknowledgement of unmet clinical need.

The penetration gap remains the single most important fact about this market’s future. At 0.01–0.02% of the population currently accessing a medical Cannabis prescription, the UK is a full two orders of magnitude below comparable markets. If even a fraction of the two million or more working-age UK adults currently unable to work due to long-term health conditions found relief through medical Cannabis, the economic and social implications would be profound.

What the market needs [and what the data demands] is a dose of the same rigor that patients are being held to. Standardized prescribing records. A national patient registry. Mandatory product cataloguing. Prescriber training that expands the talent pool beyond its current tiny nucleus. And, perhaps most importantly, an honest conversation about the push toward ever-higher THC – whether it serves patients, or simply serves the market.

An Inflection Point

The UK’s medical Cannabis sector is no longer an experiment. It is a €300 million industry, serving tens of thousands of patients, growing at a rate that would be the envy of almost any other healthcare sector. The H1 2025 data confirms what industry participants already know: this is real, it is significant, and it is accelerating.

What it needs now is not more growth for growth’s sake, but growth with infrastructure, data systems worthy of a serious healthcare sector, a prescriber base measured in the thousands rather than the dozens, and a product mix guided by evidence rather than by whatever patients and market forces have decided to chase.

The UK legalized medical Cannabis in 2018 with the promise that it would be available to patients who needed it. Seven years on, the private sector has made remarkable strides toward that promise. The question is whether the system around it can evolve at the same pace.

Sources: NHSBSA FOI · Prohibition Partners · Business of Cannabis · CQC · CannaMonitor · GrowerIQ · Releaf

About the Author: HCN News Team

Related Posts