Distressed Assets Are Reshaping Cannabis M&A

LOS ANGELES- Distressed assets are now driving the next phase of Cannabis M&A.

What appears on the surface to be a slowdown in deal activity is, in reality, a shift in how transactions are being structured and executed. The industry is moving away from expansion-driven acquisitions toward a more disciplined, opportunity-driven model built around distressed exits, asset sales, and balance sheet restructurings.

This is not a pause. It is a reset.

The Debt Cycle Is Forcing the Market’s Hand

Over the past several years, Cannabis operators scaled aggressively across fragmented state markets, often funded by high-cost debt, sale-leaseback financing, and repeated equity raises. That strategy worked in a capital-rich environment where growth was prioritized over profitability.

That environment no longer exists.

As debt maturities approach and refinancing options remain limited, operators are facing mounting pressure. Margins are compressed due to pricing declines, operational inefficiencies, and state-level regulatory burdens. At the same time, access to institutional capital remains constrained, particularly in the absence of federal reform.

The result is a growing pool of distressed operators who are no longer able to sustain their existing footprints.

Distressed Exits Are Becoming the Norm

The shift is already visible across the market.

The Cannabist Company has begun exiting multiple state markets while initiating restructuring processes tied to its debt load. Eaze, once one of the most well-known delivery platforms in the U.S., has gone through a distressed outcome that resulted in assets being sold off and absorbed by competitors.

Similarly, Schwazze has faced financial pressure leading to recapitalization efforts, while PharmaCann has taken steps to rationalize its portfolio and divest non-core assets.

These are not isolated events. They are signals of a broader trend.

Operators are exiting underperforming markets, selling individual licenses or stores, and restructuring their balance sheets in order to survive. In many cases, these transactions are happening quietly, without the visibility of traditional M&A announcements.

How Cannabist Used Canada to Restructure

What makes The Cannabist Company particularly instructive is how it leveraged its Canadian structure as part of its restructuring strategy.

This wasn’t just about cost-cutting—it was about using jurisdictional flexibility to reorganize the business.

First, Canada provided a legal and financial framework that is simply more mature for restructuring. With a Canadian-listed entity, Cannabist could operate within a system that allows for more structured negotiations with creditors compared to the constraints of U.S. Cannabis markets.

Second, this enabled the company to effectively ring-fence its U.S. operations. By separating distressed liabilities from core operating assets, Cannabist was able to protect higher-quality licenses and revenue-generating businesses while isolating underperforming segments.

Third, the structure created a centralized process for negotiating with creditors. Rather than fragmented, state-by-state discussions, Cannabist could pursue coordinated solutions such as extending maturities, reducing debt burdens, or converting debt into equity.

Fourth, it made asset sales more executable. With a formal restructuring framework in place, the company could exit markets and sell assets in an orderly way, rather than through disorganized or forced liquidations.

Ultimately, Canada was not the business—it was the mechanism. It provided the legal and financial toolkit to stabilize the company, facilitate asset sales, and reposition around a smaller, more focused operating footprint.

This playbook is likely to be replicated.

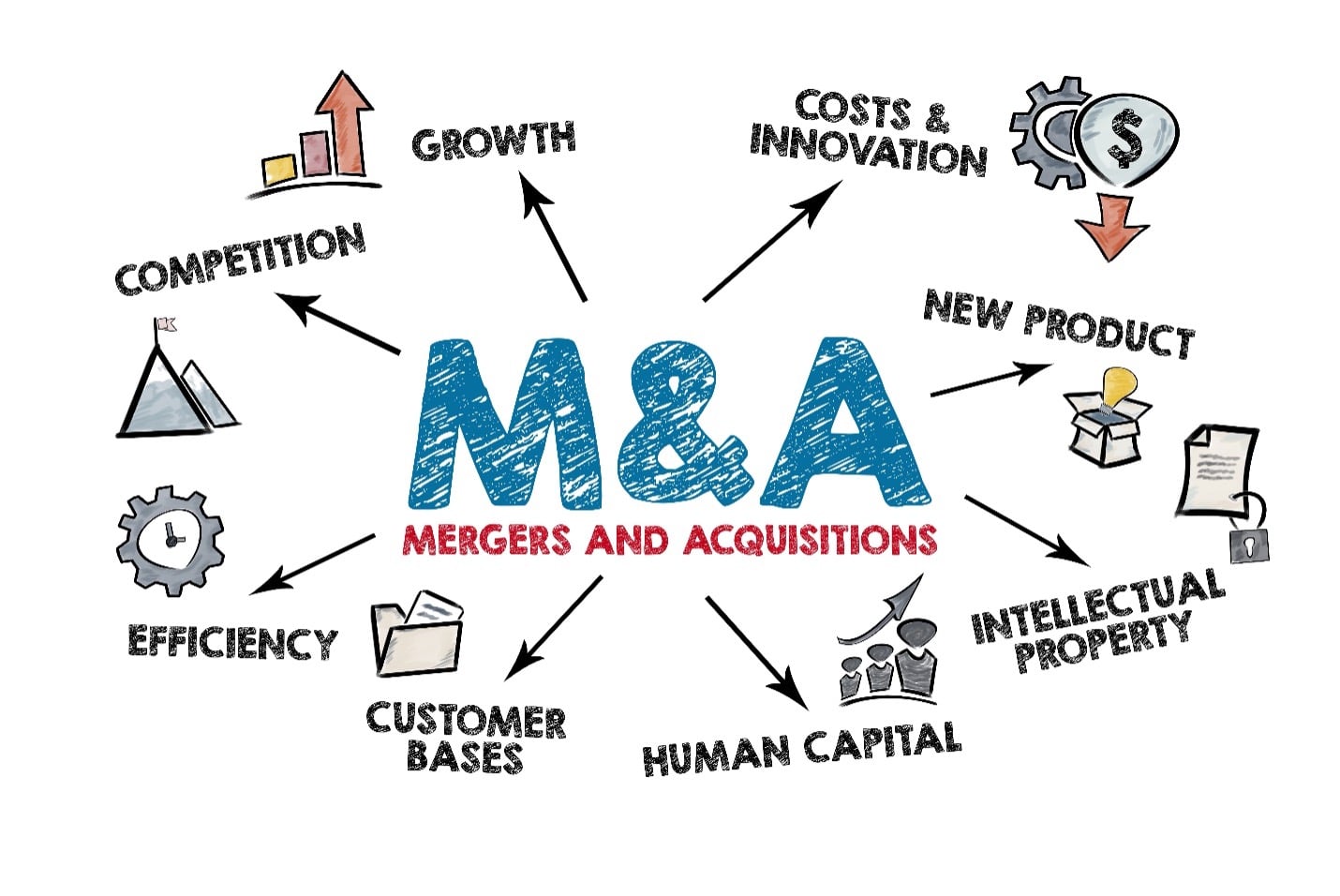

A More Surgical Form of Consolidation

Unlike previous expectations of large-scale mergers, the current consolidation cycle is playing out through smaller, more targeted transactions.

These include:

– Asset-level acquisitions rather than corporate takeovers

– Debt restructurings that convert lenders into equity holders

– Sale-leaseback transactions that unlock trapped real estate capital

– Strategic market exits to preserve liquidity

This approach reflects a more disciplined mindset among buyers, who are no longer pursuing footprint expansion for its own sake. Instead, they are focusing on asset quality, market dynamics, and operational synergies.

Highly capitalized operators are leading this shift.

With access to capital and stronger balance sheets, they are in a position to acquire assets at significant discounts—often below replacement cost. This is particularly compelling in limited-license states, where regulatory barriers create long-term value even when short-term performance is under pressure.

Valuations Are Resetting—And Opportunity Is Emerging

The repricing of Cannabis assets is one of the most significant developments in the current cycle.

Assets that once traded at premium multiples are now being sold at fractions of their prior valuations. Retail locations, cultivation facilities, and licenses that required substantial capital investment to build are changing hands at steep discounts.

For buyers with liquidity, this creates a rare opportunity to build scale efficiently.

For sellers, it represents a forced recalibration of expectations.

This dynamic is accelerating the transfer of assets from stressed balance sheets to operators with the capital and discipline to deploy strategically.

What the Next Phase Looks Like

The Cannabis industry is moving toward a more rational structure, but the path will not be uniform.

Consolidation will continue, but it will remain uneven across states due to varying regulatory frameworks, pricing environments, and competitive dynamics. Operators that understand these local nuances will have a distinct advantage.

At the same time, capital efficiency is becoming the defining characteristic of successful operators. Growth for the sake of growth is being replaced by a focus on profitability, cash flow, and return on invested capital.

Distressed assets will remain central to this transition.

They are not just a byproduct of market stress—they are the mechanism through which the industry is reorganizing itself.

The New Definition of a Winner

The last phase of Cannabis was defined by rapid expansion and market entry. The next phase will be defined by disciplined capital allocation.

The companies that emerge strongest will not be those that scaled the fastest, but those that maintained balance sheet strength and are now positioned to acquire high-quality assets under pressure. They will be the highly capitalized operators who can act decisively while others are forced to sell.

Follow Highly Capitalized Network-HCN for more Cannabis business and finance insights.

About the Author: HCN News Team

Related Posts