Greewave Advisors Analysis: Cannabis Companies & Cash Flow – Size Matters

- Over the past 6 years (2019-2024), the Tier 1 Multistate Operators (MSOs) have generated $2.3B in Cash Flow from Operations (CFO); Assuming all unpaid 280E related tax liabilities are satisfied this amount is $1.3 Billion.

- ~$1B is owed in 280E related tax among 4 of the 5 Tier 1 MSOs. Green Thumb Industries remains the outlier.

- Other than the Tier 1, CFO is insufficient to cover the punitive 280E burden and many have paused payment while the constitutionality of prohibition is being challenged in Federal court.

- Remarkably, Green Thumb Industries retains ~60% of its cash flow after satisfying its tax obligations. To put in perspective big alcohol retains about ~85%-90% but it is federally legal.

- With the inevitable reclassification to Schedule 3 (and at some point, de-scheduling), the elimination of 280E and other prohibition costs (higher cost of capital, compliance, insurance, etc.), a significant acceleration in free cash flow profiles will likely materialize industrywide.

- With 280E, it is near impossible to achieve a free cash flow yield; Green Thumb Industries and Cresco Labs are the proven exceptions.

LOS ANGELES – The inherent complexities and nuances of operating a state-regulated cannabis business are costly and arguably excessive. Capital remains scarce, and investor sentiment is seemingly lower than it has ever been, perhaps due to a lack of policy reform at the federal level as well as an overall slowdown in revenue growth (ongoing price compression, robust illicit market, rising popularity of hemp-derived intoxicants).

No question, IRS code section 280E has been the most significant drain on cash flow because businesses that sell cannabis, even in state-regulated markets, pay income tax based on gross profit, not pre-tax income. Accordingly, while most companies remain unprofitable, federal income tax is paid (or accrued). Adding salt to the wound, unlike any other corporate taxpayer, net operating losses generally cannot be carried forward to offset future taxable income.

However, a group of cannabis operators is now challenging the constitutionality of prohibition in federal court, arguing that current laws are outdated. The timing of a final ruling is unknown, but in the meantime, many have opted to pay taxes at the statutory rate and defer the incremental 280E burden. While the IRS has reiterated its position on the matter, many legal experts have weighed in, suggesting that 280E is not applicable.

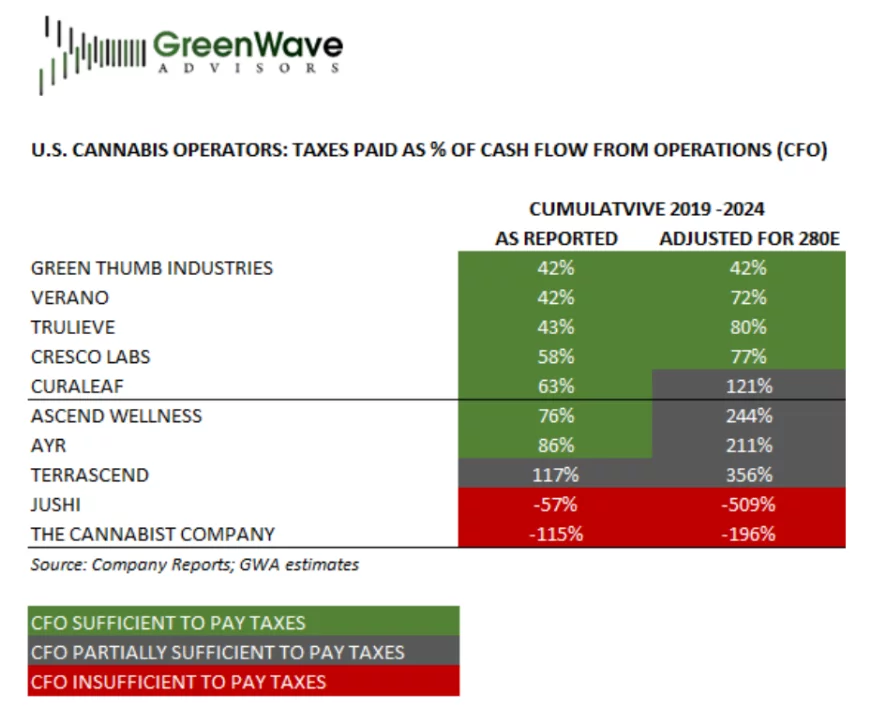

Taxes Paid as a Percentage of Cash Flow from Operations

The heat map below illustrates cash flow and taxes paid as reported for the past 6 years (2019-2024) on a cumulative basis and then adjusted assuming all unpaid 280E tax liabilities are satisfied. As noted, the Tier 1 Multi-State Operators (MSOs) have generated sufficient cash from operations over the years to pay the enormous tax burden associated with 280E. But, with all the other headwinds that come with federal prohibition, keeping up with current tax obligations is becoming more challenging, and the need to conserve cash is a top priority among operators, particularly as sources of capital remain scarce.

Green Thumb Industries (GTI) is the outlier, demonstrating incredible financial discipline over the years and able to satisfy its 280E liability in full. As indicated below, GTI retained ~60% (paid 42% in taxes) of the cash it generated over the past 6 years. To put this in perspective, Big Alcohol retains about 85%-90% of its cash flow.

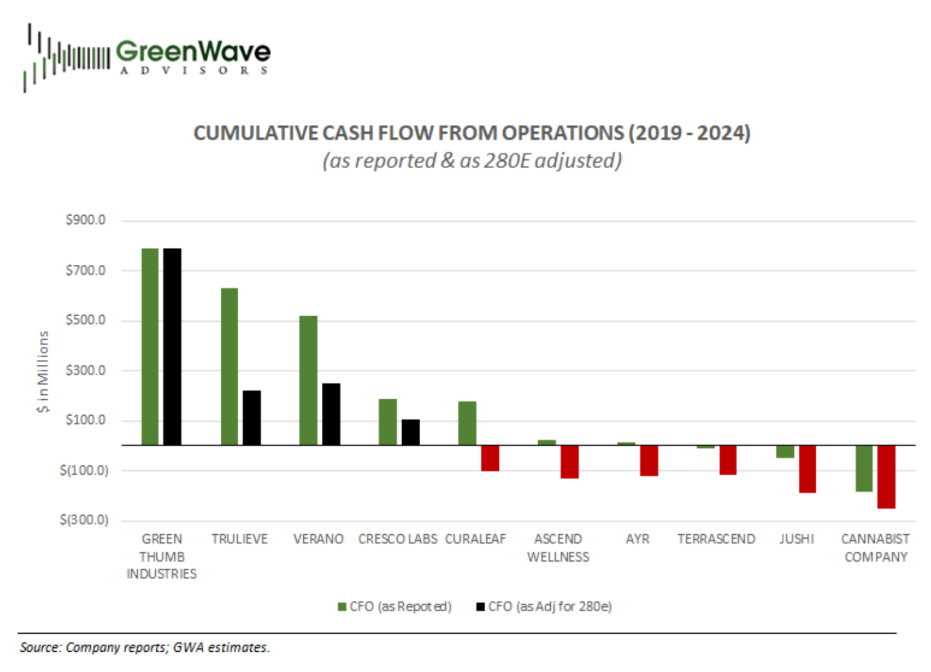

Cash Flow from Operations as Reported and as Adjusted for 280E

The following illustrates the cumulative cash flows from operations as reported and as adjusted for 280E, underscoring the vulnerability to the unpaid 280E burden. Because Curaleaf and Cresco Labs halted 280E-related tax in Q2:24, 75% of its 2024 280E is used in these calculations (i.e., the full year is realized: Q4:23 paid in Q1:24 plus 75% of 2024).

Suffice it to say that if the IRS position is sustained, it would likely not seek an immediate payment in full but rather establish an installment option, similar to Statehouse Holdings in pursuing its uncollected taxes.

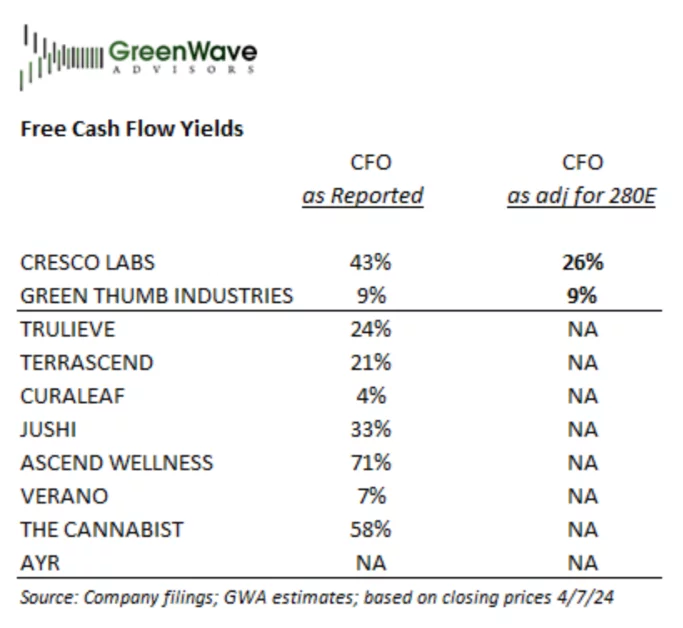

280E and Free Cash Flow Yield

To state the obvious, 280E has a material impact on Free Cash Flow yield. Assuming unpaid 280E is satisfied, Green Thumb Industries and Cresco Labs are the only operators that offer investors an FCF yield. With the elimination of 280E and other prohibition costs (higher cost of capital, compliance, insurance, etc.), industrywide, a significant acceleration in free cash flow profiles will likely materialize.

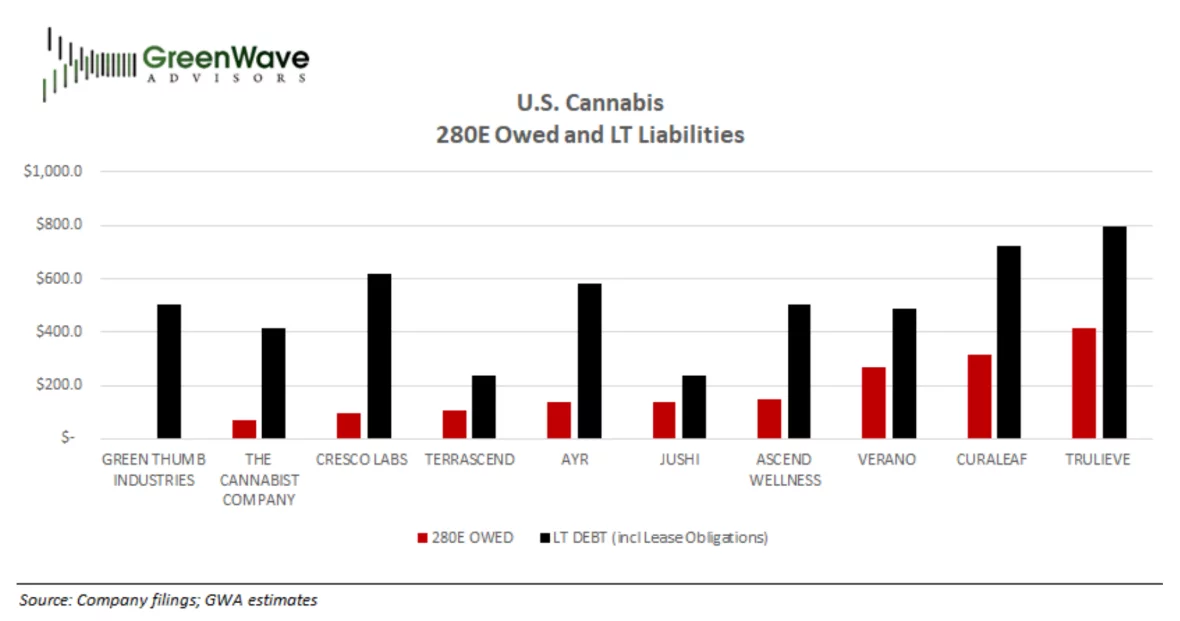

Should Unpaid 280E Liabilities Be Included in Total Debt?

Finally, this chart illustrates the unpaid 280E liability and Long-Term Debt. The incremental burden associated with this tax could have a material impact on leverage and creditworthiness.

Matthew (Matt) Karnes is the founder of GreenWave Advisors (2014) which provides financial research, analysis, due diligence and other consulting services for the cannabis industry. Matt also founded GreenWave Capital Partners (2023), an affiliate partner of Stonehaven, LLC, a SEC Registered Broker Dealer and FINRA Member Firm. Stonehaven provides services to institutions with private placements, PIPE transactions, secondary market block trades, buy-side and sell-side and merger and acquisitions.

Matthew (Matt) Karnes is the founder of GreenWave Advisors (2014) which provides financial research, analysis, due diligence and other consulting services for the cannabis industry. Matt also founded GreenWave Capital Partners (2023), an affiliate partner of Stonehaven, LLC, a SEC Registered Broker Dealer and FINRA Member Firm. Stonehaven provides services to institutions with private placements, PIPE transactions, secondary market block trades, buy-side and sell-side and merger and acquisitions.

Matt has over 30 years of diverse finance and accounting experience. Prior to founding GreenWave Advisors LLC, Matt worked in equity research focusing on the Radio Broadcasting and Cable Television industries for First Union Securities. Matt also covered Satellite Communication at SG Cowen and in addition, worked with the top ranked Consumer Internet analyst at Bear Stearns & Co – this team was consistently recognized by the Institutional Investor’s “All America Research Team”. As a sellside equity analyst, Matt authored and co-authored numerous emerging industry research reports including such names as Google, Sirius, XM Satellite Radio, DIRECTV and EchoStar Communications.

Matt was also Principal and Senior Equity Analyst at Bull Path Capital Management, a New York City based hedge fund, where he was responsible for investment strategies of emerging technologies primarily within the Technology, Media and Telecom sectors. Prior to his career on Wall Street, Matt held various finance and accounting positions at Price Waterhouse Coopers and Deloitte as well as at Texaco Inc. where he worked throughout the U.S., Europe, The Caribbean and Asia. Additionally at Chase, Matt was responsible for implementing the bank’s corporate accounting policies on commodity, interest rate and foreign currency derivative products. Matt graduated from Fordham University with an MBA in finance and earned a B.S. Business Administration with a double major in accounting and finance from Miami University (OH). Matt is also a Certified Public Accountant.

About the Author: HCN News Team

Related Posts